Samuel Buchan ,

November 2, 2022

Issue Brief: Distillate Disaster

Key Takeaways

The Biden Administration’s war on American energy continues to exacerbate supply-side constraints throughout the economy, with severe ramifications for consumer prices and industrial and agricultural output, contributing to record inflation.

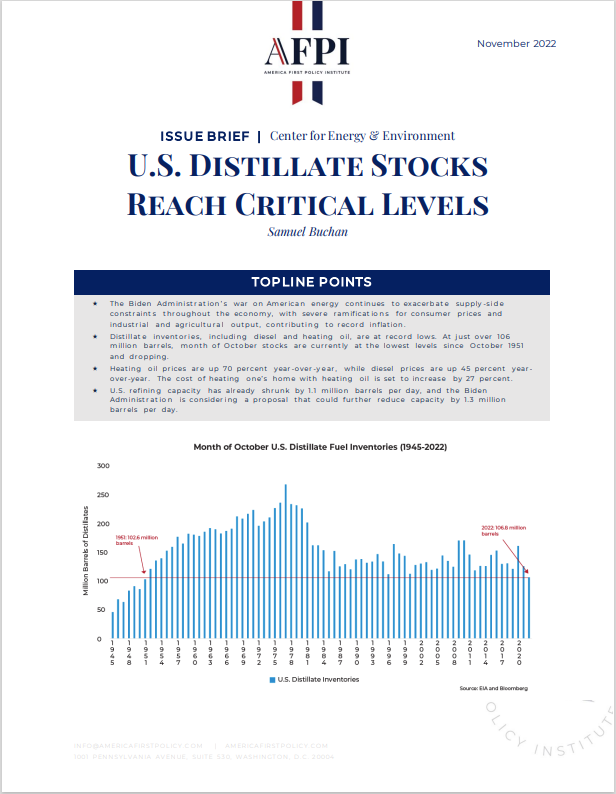

Distillate inventories, including diesel and heating oil, are at record lows. At just over 106 million barrels, month of October stocks are currently at the lowest levels since October 1951 and dropping.

Heating oil prices are up 70 percent year-over-year, while diesel prices are up 45 percent year-over-year. The cost of heating one’s home with heating oil is set to increase by 27 percent.

U.S. refining capacity has already shrunk by 1.1 million barrels per day, and the Biden Administration is considering a proposal that could further reduce capacity by 1.3 million barrels per day.

As the winter heating season closes in, our Nation is increasingly unprepared compared to previous years. Since our May 2022 report on the emerging crisis, U.S. distillate inventories, including diesel and heating oil, have continued their downward trajectory (Buchan, 2022). The latest Energy Information Administration (EIA) inventory report indicates that U.S. commercial stocks stand at just 106 million barrels, a 15 percent reduction year-over-year. That amount is only 25 days of U.S. consumption (EIA, 2022). While distillates merit specific consideration, the crisis of U.S. stockpiles cannot be separated from the overall crisis of the Biden Administration’s war on American energy. The solutions are consistently similar—reestablish confidence in the energy sector, from investment to production to refining.

The Case of America’s Depleting Distillate Stocks

The costs of diesel, included in the cost of transporting goods, fueling industrial and agricultural operations, transporting waste for major metropolitan areas, and much more, have sustained record-high prices throughout 2022. Year-to-date prices for diesel have averaged above $4.98 per gallon, compared to an average of $3.28 per gallon in 2021 during the immediate pandemic recovery and just $3.05 per gallon in the pre-pandemic conditions of 2019 (EIA, 2022).

The cost of heating one’s home is similarly concerning, with increases reflected in everything from electricity to natural gas. Heating oil is experiencing the more severe cost increase, carrying dire effects for the 4 percent of Americans dependent upon the fuel. Heating oil costs heading into the winter season stand 70 percent above 2021 prices or 93 percent above 2019 prices. Heating oil was recorded at $5.72 per gallon as of October 2022 and still rising (ibid). According to the U.S. Energy Information Administration’s Winter Fuels Outlook, heating oil will cost between 15-40 percent more for American households, depending on the severity of the winter (EIA, 2022). The base case envisioned by EIA projects a 27 percent cost increase, which equates to approximately $2,350 in total household spending throughout the six-month heating season. The United States has not entered the winter heating season with low distillate stocks or prices this high in the history of EIA-recorded inventories.

The Pandemic, Russia, and the War on American Energy

To fully understand the genesis of this shortage, we must start with the impacts of the pandemic-induced demand destruction. At the onset of the pandemic, the capital expenditure of leading hydrocarbon companies underwent significant downward revision, with the average reduction among majors totaling approximately 20 percent (IEA, 2020). The collapse in demand, beginning in February 2020, also expedited a global refining capacity loss of over 3 million barrels per day (mb/d) of operational capacity (Gerson et al., 2022), with 1.8 mb/d lost in 2021 alone—the first net loss of refining capacity in 30 years (IEA, 2022). The United States alone accounts for more than 1 million barrels per day of this lost capacity—the domestic equivalent of 5 percent of total U.S. capacity. The pandemic also triggered the largest ever recorded annual decrease in global refinery utilization, which bottomed out at 74 percent (BP, 2022). Moreover, the International Energy Agency’s (IEA) 2022 World Energy Outlook outlines a durable near-term crisis. According to the assessment, global demand by 2025 will increase by 2.6 mb/d, requiring an additional refinery throughput expansion of more than 6 mb/d. Only 4.2 mb/d are planned to be added globally. Demand for refined products by 2030 is expected to increase by eight mb/d above 2021 levels to 100.8 mb/d (IEA, 2022). The ability of refineries to return to operations once closed takes significant investment and years—typically, the decisions of refineries are planned as much as a decade in advance. Meanwhile, U.S. investment into capacity expansion or new refining capacity has been on a downward trajectory for years in the face of mounting regulatory burdens, particularly under the National Environmental Policy Act (NEPA) and the Clean Air Act (CAA). In contrast, the Middle East and Southeast Asia have continually increased investments, with China and India leading the pack (ibid).

The imposition of embargoes and sanctions on the world’s third-largest producer of crude oil and petroleum products, Russia, has undoubtedly spurred significant upward pressures on prices around the globe. For instance, since Russia’s invasion, Western sanctions have decreased global market liquidity for refined products by 600,000 barrels per day. In 2021, Russia accounted for 15 percent of global trade in refined products (IEA, 2022). This, as well as key factors like market uncertainty surrounding the scope of western sanctions and the loss of billions in assets following corporate divestment from Russian joint ventures, not to mention the sudden need to shift crude oil and petroleum product supply chains, are all compounding energy inflation. Yet further cost increases are looming around the corner, impacting economic growth projections, particularly for import-dependent Europe. In December, EU sanctions on Russia will expand to include as much as 3 million barrels per day (mb/d) of Russian seaborne crude-oil deliveries (EIA, 2022; WEF, 2022). Three months later, in February 2023, the EU will expand its sanctions regime further to include prohibitions on Russian petroleum product imports (ibid). In terms of winter heating, sanctions on Russian imports and Russian energy weaponization are leading to greater European demand for distillate fuel as an alternative source, mainly to replace natural gas. In order to fill the void of Russian volumes, the European Union is scrambling to identify alternative supplies on the market, placing significant upward pressure on petroleum costs as more countries compete for fewer resources. From the perspective of the United States, the impact of embargoes on Russian energy has led to U.S. consumers identifying alternative supplies for distillate imports. In 2021, 20 percent of U.S. imports of petroleum products came from Russia (EIA, 2022).

Under normal market conditions, one might anticipate plans for future investment and recovery in refining capacity and output, but these are not normal market conditions. Rather than restoring primacy to energy affordability and reliability, the administration appears to be casting sound, pro-growth energy policy to the wind. Look no further than the Biden Administration’s National Security Strategy, which identifies climate change as “the existential threat of our time.” While the Biden Administration can be credited for making a bad situation exponentially worse, the U.S. refining sector has been inordinately burdened by increasingly outdated and cumbersome regulations dating back to the 1970s—when the last new refinery was built. These include NEPA and CAA, which combined levy layers of regulatory red tape and construction costs on proposed new refining capacity buildouts. Renewable Fuel Standards, an alternative fuel regime established in 2005, also amount to a “hidden tax on consumers and refiners” (Brooks, 2022). These standards force refineries to either blend less efficient and dirtier renewable fuels or purchase renewable fuel credits, compounding the cost of refining. As of 2020, renewable fuel credits amounted to a $30 billion market—$30 billion that could have been reinvested into refinery upgrades, expansions, or new builds (ibid). This is what Larry Kudlow, former Director of the National Economic Council, has dubbed the “wet blanket over the entire oil and gas industry.” Yet there are more “wet blankets.” Due to the broad adoption of environmental, social, and governance (ESG) standards—the manifestation of a regressive economic philosophy known as stakeholder capitalism—investors and companies within the hydrocarbon sector have experienced limited access to the flow of capital toward much-needed infrastructure development, capacity expansion, and essential upgrades and repairs.

Moreover, the actions of the congressional Left and the Biden Administration in advancing approximately $1.5 trillion in climate-related spending throughout 2021 and 2022 have further distorted markets and inflamed negative incentives for hydrocarbon production recovery and growth. For instance, the IEA’s 2022 World Energy Outlook outlined a global forecast based on the declared policies and global emission reduction pledges. Under this envisioned scenario, refining capacity is continually under threat of closures. While this assumes a transition to alternative transportation and heating fuels, it does not adequately account for the slow and complex effort of radically overhauling national transportation, industrial, and residential sectors to run solely on electrons rather than hydrocarbon molecules. This not only hurts the hydrocarbon sector, but it hurts American consumers by artificially increasing prices and lowering their standard of living. By contrast, America First policies advanced under the Trump Administration, such as efforts to modernize permitting to accommodate supply-side growth, caused energy production to reach new levels, establishing the United States as the leading producer of crude oil and refined petroleum products (EIA, 2022; Enerdata, 2022).

Implications and Solutions

Absent corrective actions by policymakers and the capital investment community, the global economy will continue to be hampered by heavy-handed government interventionist policies and the collateral damage of necessary, albeit costly, sanctions on Russia. Corrective action is essential, particularly when the United States is sustaining record inflation driven mainly by energy inflation and supply-side constraints—the most recent Bureau of Labor Statistics’ Consumer Price Index registered U.S. inflation for the previous 12 months at 8.2 percent in September (BLS, 2022). Further cost increases within the energy sector, namely crude oil and its refined products, will continue to be a key driver of inflation in the coming months. This winter, Americans will not only be facing the sustained inflation of groceries and nearly every other household good but also the rising costs of heating their homes, regardless of their fuel source. The heating oil crisis, in particular, will levy additional pressures on households during the heating season, particularly in New England. This region’s opposition to natural gas pipelines leaves communities with few reliable heating alternatives.

In May 2022, our report on the then-developing distillate crisis warned against implementing policies that failed to anticipate and mitigate the consequences of embargoes—namely, those that demonstrably put pressure on the ability to produce and transport hydrocarbons. The same is true today, particularly in advance of further sanctions on Russian energy this coming December. Americans cannot afford a regime of ad hoc and insulated policymaking. To address the American economy’s vulnerabilities to current and future energy crises, the current administration must overhaul regulations and permitting challenges impacting hydrocarbon development. To restore upstream operations and market certainty, the administration should remove its opposition to new production on federal lands, work with the Federal Energy Regulatory Commission to permit pipeline construction and expansion, and halt releases from the Strategic Petroleum Reserve that only undercut the price incentive for producers.

Regarding downstream operations, the administration should curb the Environmental Protection Administration’s mandates on renewable fuel credits for refineries that add to refining and consumer costs. More importantly, and impacting all hydrocarbon operations, Congress should overhaul outdated regulatory regimes like NEPA and CAA to make it easier to build everything from rigs to pipelines to refineries in America. Finally, and more immediately, the Biden Administration should reverse the implementation of discretionary fiscal policies, including those aligned with ESG standards, that are openly declared to cause the end of hydrocarbons. Such policies only distort the long-term financial planning of American producers, refineries, and retailers to the disadvantage of American energy independence and security.

Unfortunately, after years of underinvestment and distortionary or outright hostile policy, even these measures will have little impact on the immediate availability of U.S. distillates. To address the diminishing capacity of U.S. refining, The administration’s myopic focus on renewables also delivers false hope that those resources are available and ready at the scale necessary to replace hydrocarbons. The challenges of electrification in the transportation sector, particularly diesel-dependent commercial transportation and agriculture, are key examples. Facilitating greater and more readily available access to capital for the U.S.-based hydrocarbon sector will ensure that the United States, not China, will be the world’s largest source of refined products.

Despite the repeated calls from Americans and our allies for more significant volumes of U.S. crude oil and refined products to offset the loss of Russian fuel, the Biden Administration continues to enact its ideology-driven agenda rather than operating within the economic and political landscape of today. For instance, the Biden Administration has engaged in economic and political brinksmanship with the world’s second-largest petroleum-producing nation, Saudi Arabia, rather than addressing America’s domestic ability to resolve the global energy crisis or collaborate with strategic partners constructively. Undoubtedly, as the Biden Administration is deliberating, imposing an export ban on refined products is not the solution. An American Council for Capital Formation study found that such an export ban would further reduce our already stifled domestic refining capacity by an additional 1.3 mb/d (ACCF, 2022). Just as significant, such a ban could slash U.S. GDP by more than $44 billion next year and eliminate as many as 85,000 American jobs. This loss is representative of the proportion of U.S. refining capacity that is geared toward supplying global demand.

U.S. distillate stocks are one example of the implications of policies that overlook the market dynamics of hydrocarbons. We are far from a transportation sector powered by electrons rather than refined petroleum products. The focus on green utopian values has restricted access to capital for refinery repairs, upgrades, and construction. It has made supporting infrastructure that is essential to deliver affordable and reliable energy politically untenable, particularly along the Pacific and Atlantic seaboard. Policy does not operate in a vacuum, and the plausibility of a distillate shortage this winter season will further cripple the ability of lower- to middle-class families to maintain their safety, let alone a positive economic outlook. Given a choice, Americans will overwhelmingly choose to improve their families’ living standards ahead of climate ideology.

Works Cited